Surviving Trust Tax Season 2025 – And Beyond

“Trustees remain accountable for all tax matters of a trust, regardless of the economic activity of the trust.” (SARS)

The official trust filing season for the 2025 year of assessment is now open for both provisional and non-provisional taxpayers – and SARS has issued stern warnings to trustees to fulfil their tax obligations.

Who must file trust tax returns?

A trust is included under the definition of a “person” in terms of the ITA (Income Tax Act no.58 of 1962) and is therefore regarded as a taxpayer.

All South African trusts, including resident and non-resident trusts, that are registered for income tax, must file a tax return annually, even if the trust is not economically active.

A trustee is the representative taxpayer of a trust. Trustees or representatives must register the trust for income tax and file the required tax returns annually. Alternatively, a registered tax practitioner can be appointed as the representative taxpayer.

What must be done?

Taking into account recent changes to the legislation, trustees must submit their returns for the 2025 year of assessment and file the mandatory supporting documents listed further below.

Recent legislative changes

- The “flow-through” principle is now limited to resident beneficiaries, so all amounts vested to non-resident beneficiaries are taxable in the hands of the trust. This also affects the submission requirements for provisional tax (IRP6).

- Foreign tax credits for taxes paid on income or capital gains earned in a foreign jurisdiction can now be used to prevent double taxation.

- From the 2025 tax year onwards, unused foreign tax credits will be carried forward automatically to the subsequent years of assessment, up to a maximum of six years.

- The Section 12H Learnership Agreement is extended to 31 March 2027.

- The definition of a trust is updated to include collective investment scheme portfolios.

- SARS has issued new rules on how losses relating to distributions are limited under section 25B.

Return submissions

The final deadline for the submission of provisional and non-provisional Trust Income Tax Returns (ITR12Ts) is 19 January 2026.

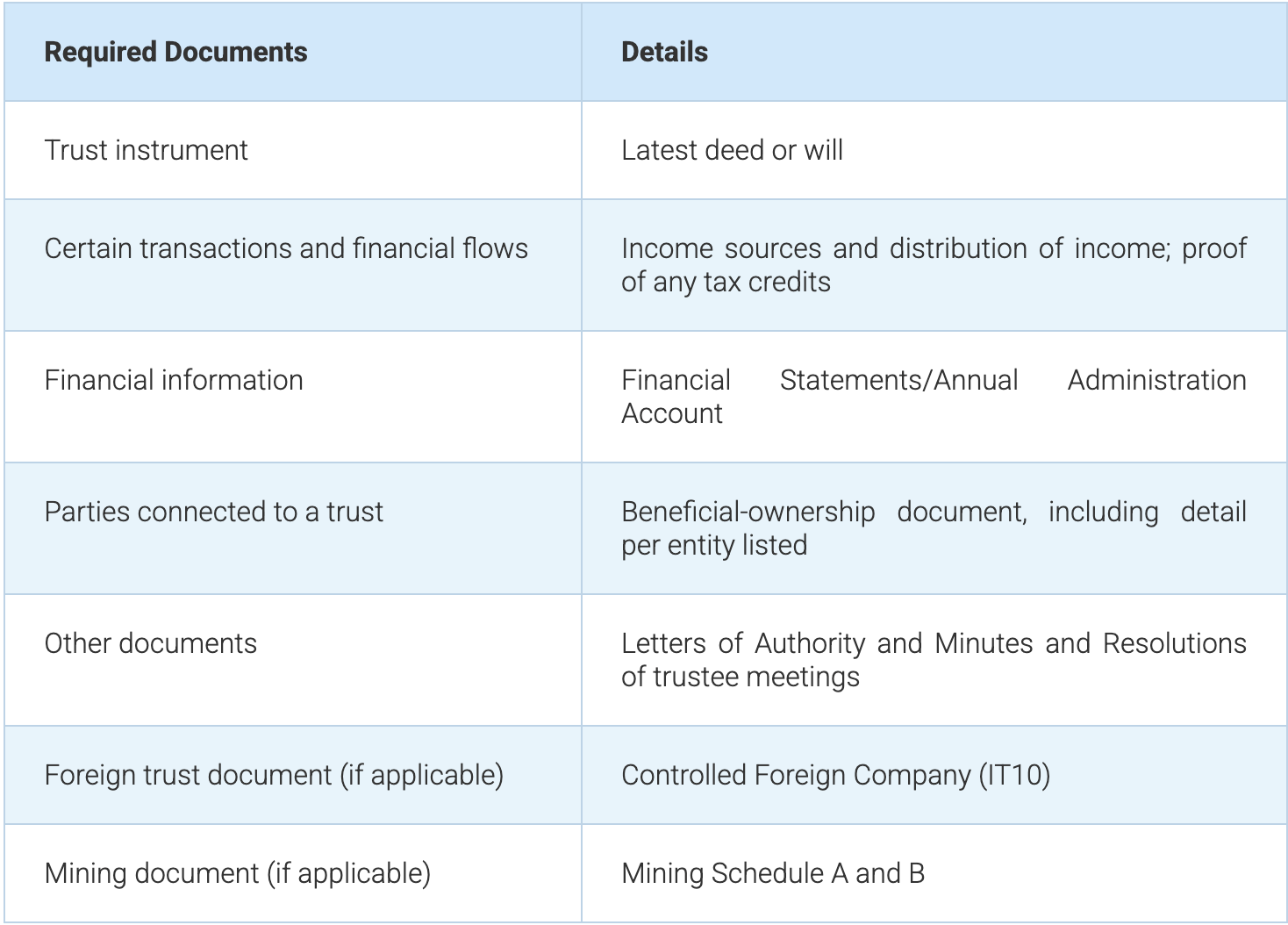

Mandatory supporting documents

Source: SARS

File on time!

Trustees and administrators should take note that all the return submissions and supporting documents are due by 19 January 2026 – just days into the new year.

Submitting within the deadlines is necessary to comply with SARS regulations. Late submissions can lead to administrative penalties, interest charges, and additional steps.

What else must be done?

Because a trust is also a provisional taxpayer, trustees should be aware that a trust is further required to submit provisional tax returns (IRP6) twice a year in August and February.

In addition, trustees are also required to submit an IT3(t) third-party data return that provides details of amounts vested to beneficiaries.

Finally, all income derived from a trust must be declared by any resident beneficiaries of trusts in their own income tax returns.

Looking ahead: Key tax dates for trusts

- 19 January 2026: Final deadline for provisional and non-provisional trust tax return (ITR12T) submissions.

- 28 February 2026: Second provisional tax payment for the 2026 assessment year.

- 31 August 2026: First provisional tax payment for the 2027 assessment year.

- September 2026 (date TBC): Opening date for Income Tax Returns for Trusts (ITR12T) submissions for 2026.

- 30 September 2026: Deadline for IT3(t) return submissions for trusts which declare amounts vested to beneficiaries’ income.

- 30 September 2026: Top-up provisional tax payment for the 2027 assessment year.

Consequences of non-compliance

SARS takes a zero-tolerance approach to taxpayers who do not register for the applicable tax, file tax returns, declare income accurately, or pay their tax debt.

Non-compliance with these obligations is a criminal offence and will attract penalties and interest.

Surviving Trust Tax Season 2025 and beyond

Never fear! Our team is well experienced in keeping trusts compliant throughout the year. We don’t just contain costs and prevent hassles with the taxman; we also provide peace of mind.

If you need assistance meeting the next trust tax deadline on 19 January 2026, simply reach out to us. It’s the easiest way to survive this trust tax season and those ahead.